The first quarter of the year was the perfect teaser to what the hybrid life could look like going forward- with the Omicron variant on the decline, restrictions being eased, masks coming down, and people alternating between meeting across tables and Zoom links. This was all quite symbolic as we approached the 2-year COVID anniversary in March. Nevertheless, it felt great to be able to participate in offline experiences again- whether it was grabbing a meal with colleagues, listening to a founder pitch, or participating in events (more on that below).

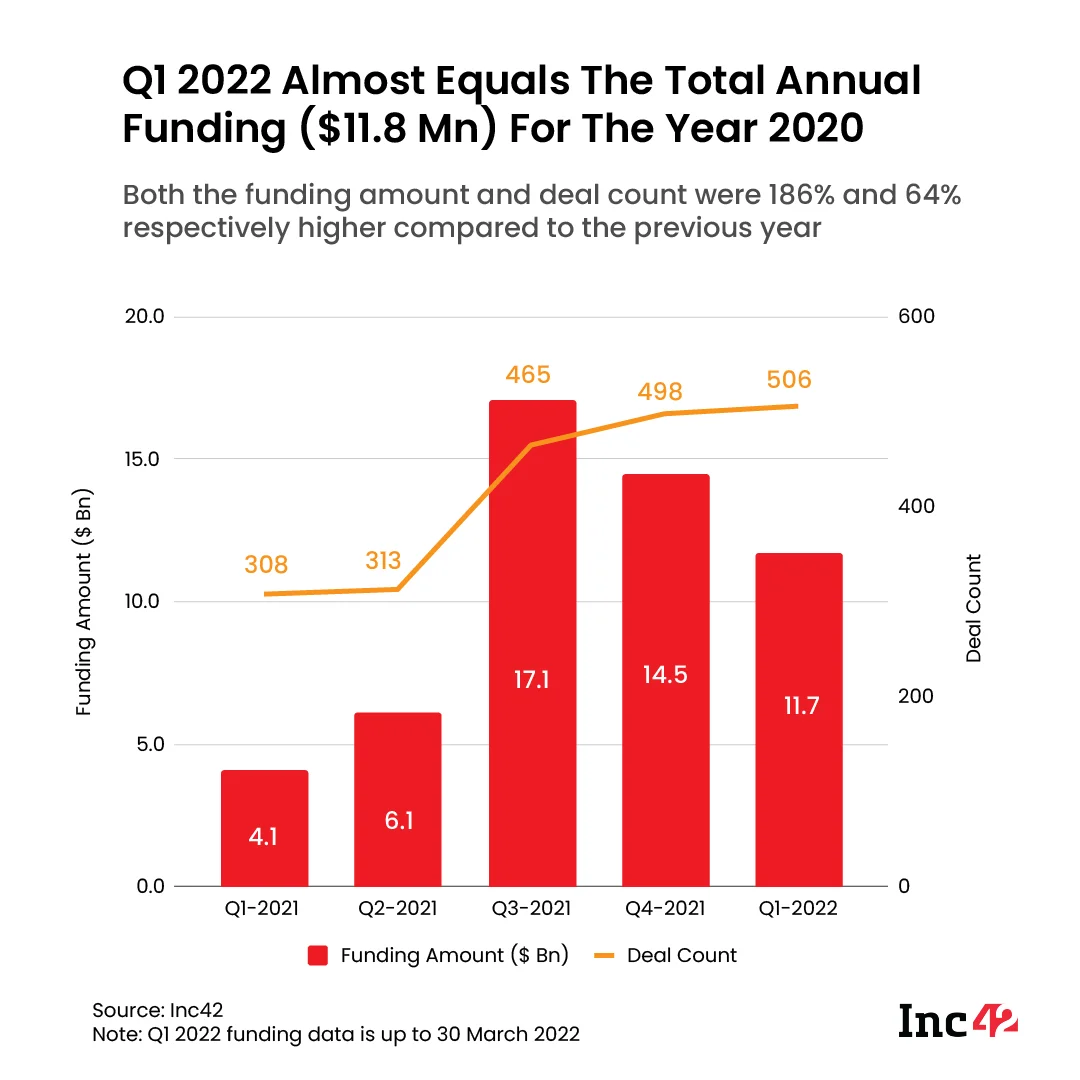

From a business perspective, the quarter has been humbling- the bull run in the public and private markets slowed down, with the pace and quantum of fundraising taking a breather in Q1. Despite the slowdown, the Indian startup ecosystem has truly come a long way- funding raised in Q1CY2022 (~$11.4BN) was almost equal to the entire funding raised by startups in CY2020.

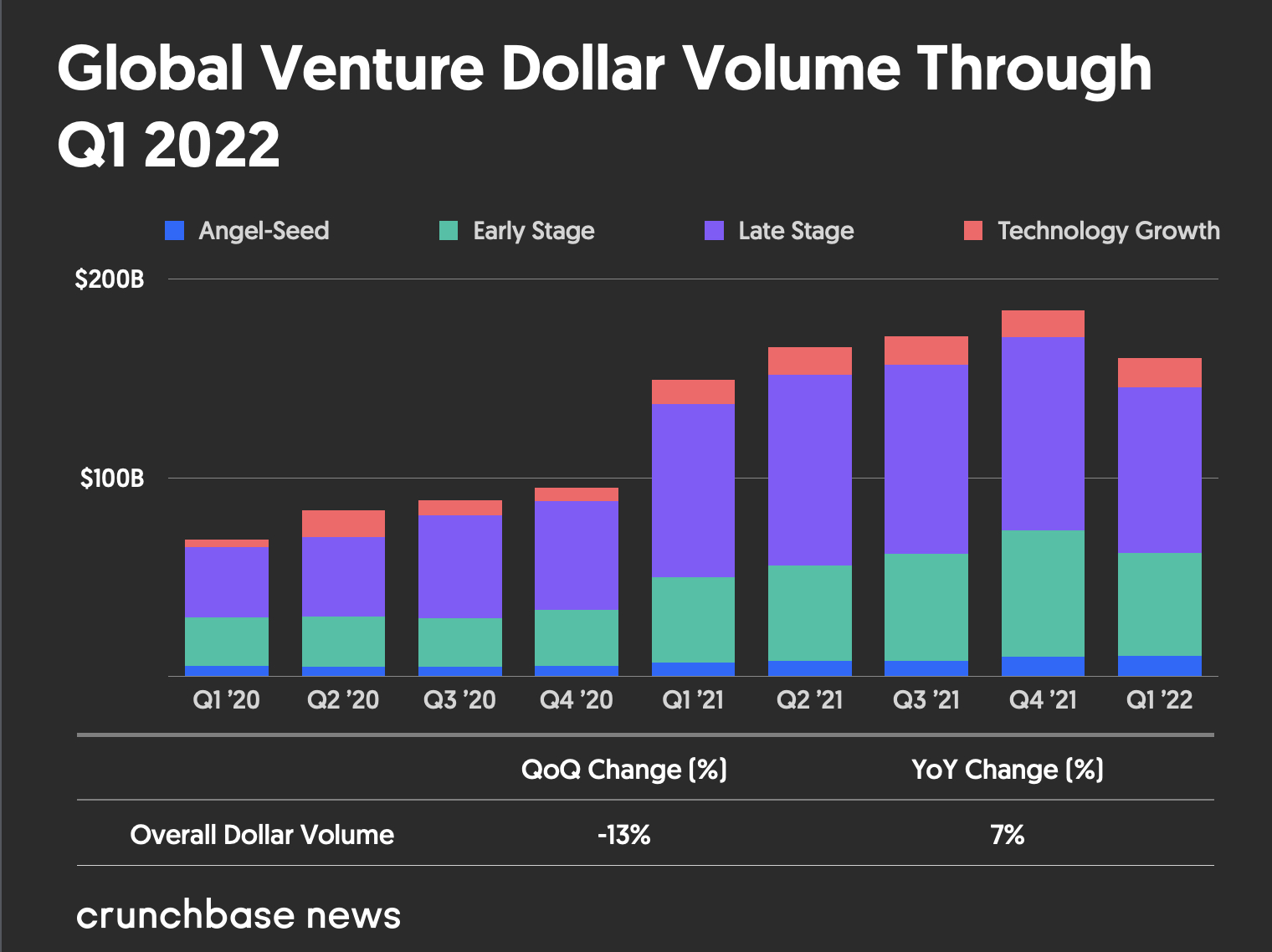

2021 definitely left its mark on the global VC ecosystem- Venture funding almost doubled to $669BN in 2021 from $335BN in 2020. This momentum in funding that 2021 brought with it, slowed down in Q1CY22. This quarter the global VC funding reached $160BN, up 7% YoY, but down 13% QoQ. This marked the first time in a year of records when startup capital fell quarter over quarter. While this shows de-growth, we believe it’s still too soon to call it a puncturing of the bubble: despite the slowdown, Q1CY22 marked the fourth-largest quarter for funding on record.

2021 has been a landmark year for the Indian startup ecosystem. Tech unicorns grew at a record pace: it took 2 years to create 40 unicorns in 2010, it took a mere 11 months in 2021. Even on the exits front, they have been dispersed across companies in 2021 unlike 2016-2020 where Flipkart accounted for the majority of liquidity. There are big changes coming owing to the dearth of tech contribution to the NIFTY50- Reliance has already invested $20BN behind Jio and acquisitions are growing as an avenue for exits for the new-age and legacy companies alike.

.png)

Moving on to Q1CY22, in line with the global ecosystem, a similar trend was observed in India- startups raised an incredible $11.4BN in the first quarter, up 185% YoY but down 24% QoQ. But the question is why this slowdown? Short answer: a bunch of unfortunate events happening at the same time. A spike in US interest rates, geopolitical tensions due to Russia’s invasion of Ukraine, fuel prices at a record high, and the crash of public markets US and India are the top contributors.

Indian public markets have also observed an end to the massive bull run of 2021. A boom in technology IPOs in India risks grinding to a halt after the largest public issue of the country, PayTM, tanked soon after listing. PayTM’s shares, which went public in November, are down 63% from listing price. Zomato, the food delivery startup, also went public this year and has seen a similar trend, albeit less drastic- its share price is down 10% from its IPO price. On the other hand, Nykaa, the beauty marketplace, is up 50% from its IPO price. Everyone in the Indian public markets now has their eyes set on the massive public share sale of the state-owned Life Insurance Corporation of India, which could dictate the course of technology companies’ listing plans. Our thoughts? We believe last year was all about greed and, short of an alien invasion, the market was ready to accept anything. Right now, fear is creeping up but give it some time, and greed will be right back.

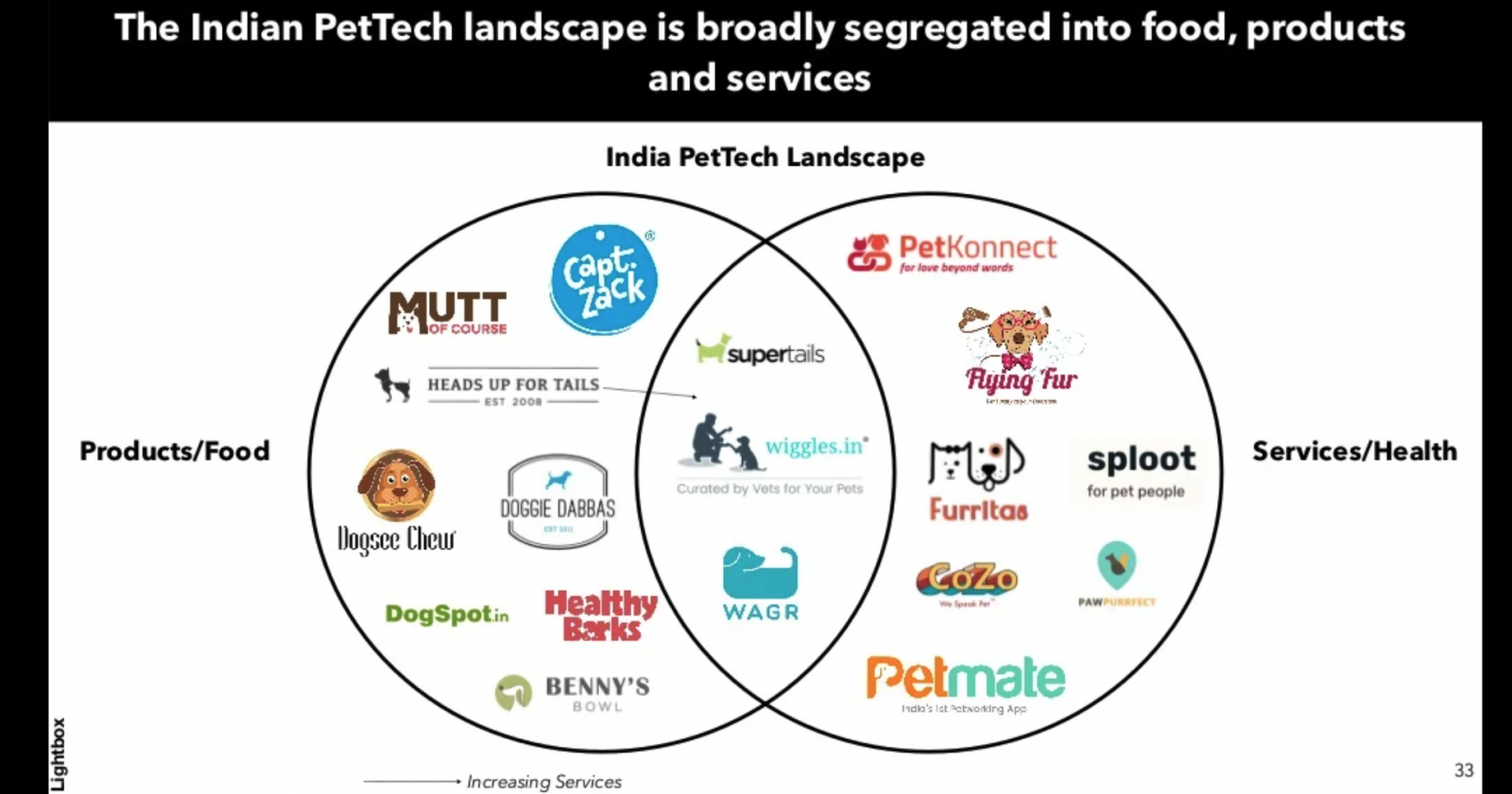

The research desk has had an eventful quarter with the team delving into 3 interesting sectors- the Pet Tech industry, Wealth Management platforms in Crypto, and NFT Gaming. Let’s look at the only non-web3 space first: Pet-Tech.

At Lightbox, we’re always iterating on the type of content we put out. For Pet Tech, instead of writing a long-form piece on our thesis, like we usually do, we figured we’d publish a deck and a short teaser we made on the space. Throughout the presentation, we tell you all about the why and the what regarding the craze of adopting pets and the funding frenzy that's following suit. Initially, we throw some light and give some credit to the pandemic (unheard of) for the increased humanization of pets, which has led to the premiumization of new products and services. Think of personalized dog meals at the click of a button or a monthly subscription treat box for your four-legged friends. We deep dive into the pet tech market in the US and understand the various components of it: food, products, services, and health. Who would have imagined that personalized fresh pet food would have received $150MM+ in funding in the last two years? Would you have ever thought that tele vet consultations would increase the average yearly vet visit 4x? Probably not! We spent time zeroing down on India and where we stand in the global context. Take the US for example- more US households have pets than children. 84.6MM U.S. households have dogs, cats, and other pets, while 35MM have children. Although India is still at a fairly primitive phase in its pet tech development, the growth in the segment is at an unrivaled 30% YoY. Click here to read our thesis and go through the presentation we made on the space. We would love to hear your thoughts on the deck!

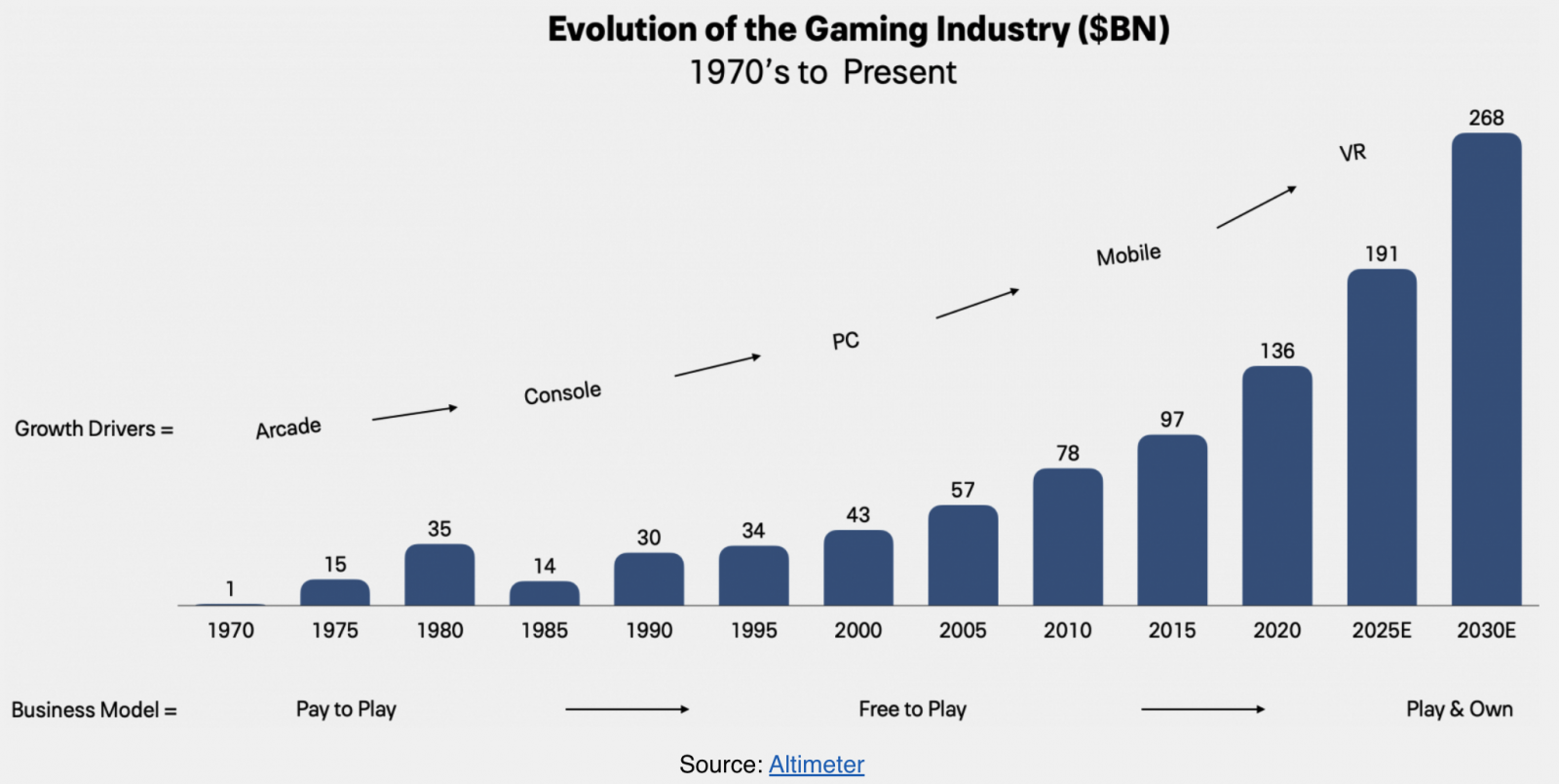

Coming back to the web3 world, we looked at one of the most exciting use cases of NFTs- Gaming. Let us put some numbers to that excitement. In 2021 NFT sales volume totaled $25BN of which nearly $3.4BN was spent on NFT in-game assets. One of the fastest-growing use cases for NFTs is gaming, Axie Infinity being at the forefront of this touched 2MM DAUs and a total of $2.3BN in total sales volume in October 2021. The business model of the gaming industry has evolved from being Pay to Play (PTP) in the 1980s → Free to Play in 2000s → Play to Earn post-2017. The mainstreaming of blockchain technology and its applications has enabled the game creators to create economies within a game while ensuring none of the fun attached to gaming is lost. This new type of game allowed for all objects within a game such as land, weapons, and skins to be tokenized as NFTs while also creating further value through their in-game token as cryptocurrencies that are owned by the gamer. As we witness the continuous adoption of P2E games, we will see better experiences being built across all categories of gaming. Currently, we have card trading, character fighting, and racing games, which are being newly created. However, we will witness AAA games such as Fortnite, Call of Duty and other multiplayer games incorporate this technology and economic model. We believe there will be some headwinds such as adoption of cryptocurrencies and regulation of all these new assets. Predicting what might happen in the future is speculative but we continue to see increased activity and development in the space. Check out our in-depth thesis on the space here.

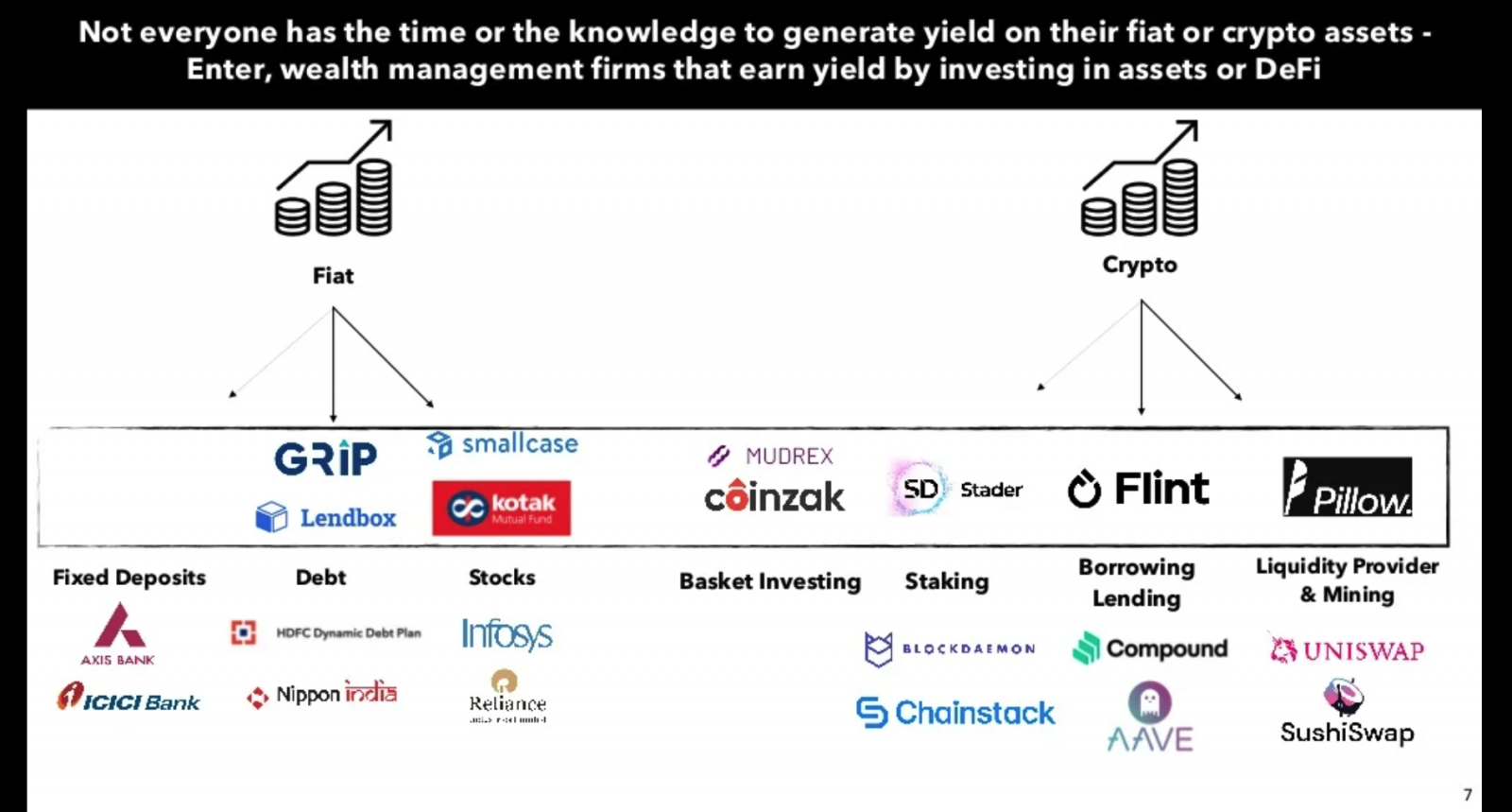

Another trend that caught our attention this quarter was the sharp increase in wealth management platforms in the Crypto world. With a lot of consumers joining the Crypto bandwagon, most of these investors don’t really understand how to generate yield on their holdings or interact with DeFi platforms due to the complex UI/UX being difficult to navigate. To understand this yield generation better, we made an in-depth deck on Wealth management in Crypto. In this, we covered the different ways that users can generate yield on their holdings such as staking, liquidity providing, P2P borrowing & lending, or investing in curated coin baskets. We deep dive into each of the concepts mentioned above to show how users can generate yield on their crypto holdings and the various annual percentage yields (APY’s) they can earn across different strategies. However, due to the complex nature of these assets and platforms, we are now seeing startups that generate yield for users by providing a seamless onboarding experience and easy to use platform for the average crypto investor. We see the number of people investing in Crypto increase exponentially over the coming years and with that the need to generate yield on their holdings. Check out our thesis on this space with our presentation here. We also spoke with an expert in the field, Martin Green, from a quantitative fund that invests in digital assets. Listen to him on our podcast here.

With COVID restrictions lifting across the country, in-person events came back to life with full force. We organized and participated in a panel in collaboration with Ladies Who Lead, empowering, mentoring, and making invaluable connections for women in the Venture Capital ecosystem. We’re looking forward to more of these in the coming months.

Talking of in-person events, this quarter we also hosted our LPs and founders at our office in Mumbai for an evening full of riveting conversations. It was great to see you all in person after so long, and to see all our founders getting a chance to interact with our investors.

It’s been a great quarter for our portfolios as well. Rebel Foods’ homegrown brand Faasos becomes the largest Indian-origin QSR chain with 500+ internet restaurants in 10 countries. WayCool unveiled the ‘most comprehensive tech stack in the food economy’ solution on the side-lines of Dubai Expo 2020. With the entry into the

We launched the 10th and final episode of our podcast, That’s Lit, wrapping up season 1. Ideating and launching this podcast has led to us having some great conversations with the leading minds of the country. Catch us in conversation with Sanjeev Bikchandani, the founder and vice chairman of InfoEdge.